Top 10 Health Insurance Companies 2021

Description

Please subscribe & share for more videos:

Subscribe: https://goo.gl/cWHPBJ

How to choose the best health insurance for your requirements

Coverage

Firstly decide on the type of coverage you require. For example, a basic hospital policy will most often cover accommodation as a private patient in a public or private hospital but exclude high-cost services like pregnancy.

Benefits

Your chosen health insurance company might use dollar or percentage amounts or both to show how much you can claim for a specific service, for example, $250 per person or 75% of the total costs. Hospital cover has been categorized into four tiers – Basic, Bronze, Silver and Gold. These tiers, each with a minimum level of cover guaranteed, will make it easier for you to compare and choose the right policy that meets your requirements.

Annual limits

A limit refers to the maximum benefit payable each year for a specific service/treatment. Annual limits differ between funds and policies, so make sure that you review the company’s Standard Information Statement (SIS).

Co-payments or daily excess

In exchange for lower premiums, hospital policies generally have co-payments, also known as an excess, wherein you agree, upfront, what amount you’re willing to pay each day you’re in the hospital. Depending on the insurer you’ll typically have the choice of zero, $250 or $500 excess.

Health Insurance Reviews

Read what customers are saying about the company, how satisfied they are with their service and how many complaints the company annually receive.

Exclusions

Carefully review which services and conditions your provider does not cover. With the new health insurance reforms where hospital policies must adhere to a simplified classification system; Gold, Silver, Bronze and Basic, your health fund might decide to exclude or include specific benefits.

Premiums

A cheap policy isn’t necessarily the right policy for you. Make sure to compare funds that provide the coverage you require before reviewing cost. This way, you’ll generally be able to find an acceptable value policy for an affordable price.

Waiting Periods

Look at the length of time you’ll have to wait before you can claim a benefit, for example, when you have a pre-existing condition, you generally have to wait 12 months. Waiting periods can range anywhere from 1 day, two months to a year and are different between insurers.

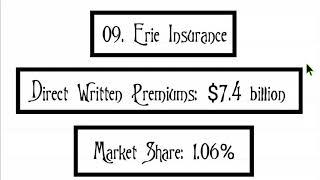

Market share

If a health fund owns more of the market, it means that they have sold more policies, which could mean that more people are trusting that particular health fund.

Comments